blog

Best Locked Goal Savings Options for People Who Keep Spending Their Savings

If you keep raiding your savings before reaching your goal, locked savings accounts and apps can remove the temptation entirely. Here's what works.

Best Locked Goal Savings Options for People Who Keep Spending Their Savings

Some people are great at setting money aside. They're just terrible at leaving it there.

The savings account fills up slowly, the goal feels far away, and then something comes up. Maybe it's a sale, a night out, a car repair, or just a low-balance anxiety that makes the savings feel better as spending money. Whatever the reason, the balance disappears, and the goal resets to zero.

If that pattern sounds familiar, the problem is not a lack of discipline. The problem is that the money is too easy to touch. A regular savings account offers no real friction between you and that balance. You can move it in thirty seconds.

Locked goal savings change that. They use real consequences, time locks, or penalty structures to make early withdrawal genuinely costly. The goal is not to punish anyone, it is to create enough resistance that impulse decisions do not win.

This article breaks down the best locked savings options available, how each one works, what makes them genuinely useful for serial savings-touchers, and how to pick the right fit.

Table of Contents

- Why regular savings accounts fail impulsive savers

- What makes a savings option genuinely locked

- Certificates of Deposit (CDs)

- Treasury Bills and I-Bonds

- Employer retirement accounts (401k)

- Goal-based locked savings apps

- Bloomin: locked savings built around consequences

- How to choose the right locked savings tool

- Common mistakes to avoid

- A simple checklist before you lock your savings

Why Regular Savings Accounts Fail Impulsive Savers {#why-regular-savings-accounts-fail}

Standard savings accounts are designed for access, not restraint. Banks want you to deposit and withdraw easily. That convenience is a feature for most customers, but it is a trap for anyone who struggles with savings discipline.

Here is the cycle most people end up in:

- Set a savings goal (vacation, down payment, emergency fund).

- Open a savings account or designate a sub-account.

- Contribute money for a few weeks or months.

- Spend the balance for something unplanned.

- Restart from zero and feel bad about it.

The savings account is not the villain here. It is simply the wrong tool for someone who needs friction between themselves and their money.

Budgeting apps, spreadsheets, and savings trackers do not solve this either. They show you the number clearly. They do not prevent you from moving it.

What actually works is removing the easy exit. If pulling the money out costs something real, time, a penalty fee, a tax consequence, the impulse decision becomes harder to justify. That is exactly what locked savings tools are designed to do.

For a deeper look at the psychology behind why touching savings is so hard to resist, the Bloomin guide on how to stop touching your savings walks through the behavioral side of this clearly.

What Makes a Savings Option Genuinely Locked {#what-makes-it-locked}

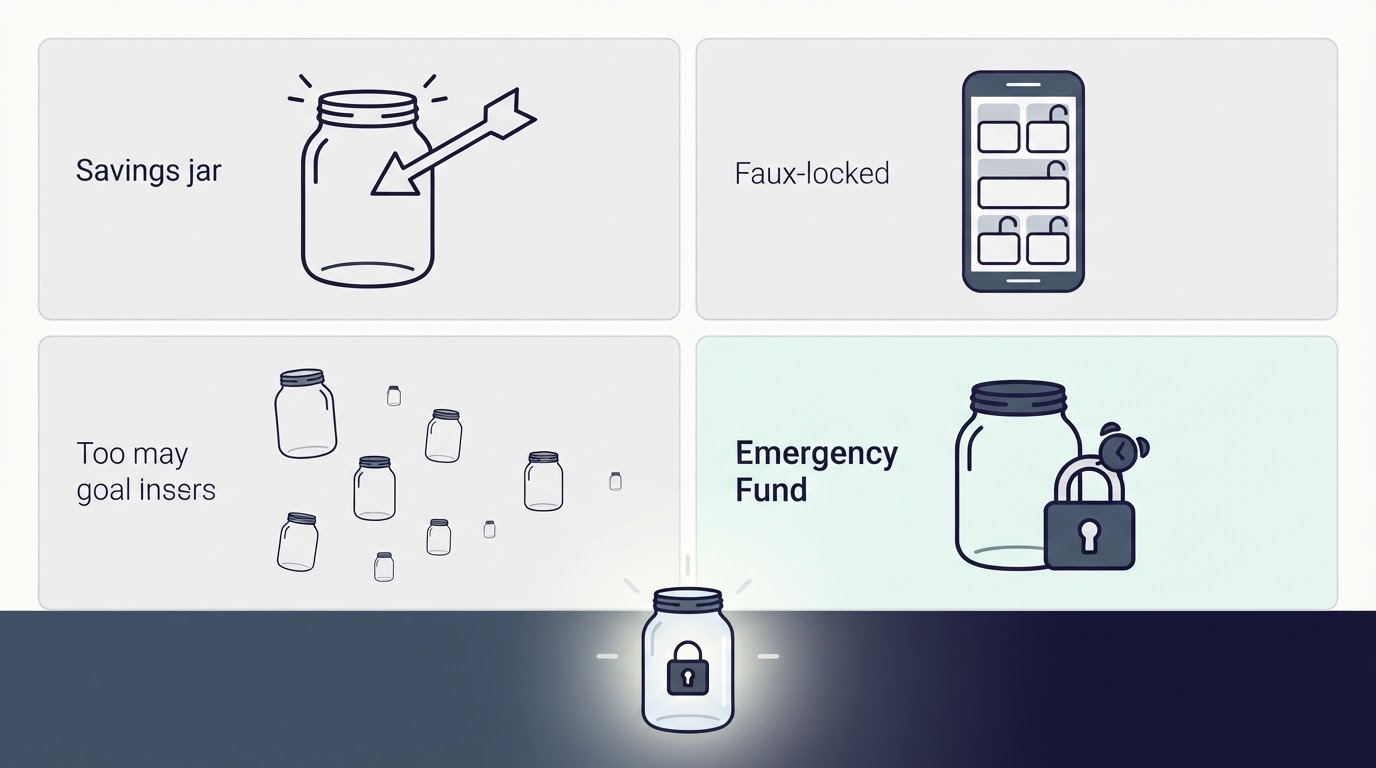

Not all "locked" savings products are the same. There is a spectrum from mildly inconvenient to genuinely penalty-heavy.

Lightly locked options make access slower. You might need to wait a few business days to transfer, or complete a few extra steps. These help a little but can still be bypassed.

Moderately locked options charge a financial penalty for early access. CDs are a good example. Break the term early and you lose several months of interest.

Strongly locked options combine a meaningful financial penalty with a named purpose. The money has a job, and walking away from that job costs real money.

The strongest locked savings tools work because they make quitting feel expensive, not just annoying. If you can withdraw in four clicks with no consequences, the lock is cosmetic.

Certificates of Deposit {#certificates-of-deposit}

A Certificate of Deposit (CD) is one of the oldest and most reliable locked savings tools. You deposit money with a bank for a fixed term, anywhere from three months to five years, and the bank pays you a fixed interest rate. You agree not to touch the money until the term ends.

Early withdrawal penalties vary by bank but typically equal three to six months of interest on shorter-term CDs and six to twelve months of interest on longer ones. That is a real cost, not a fake one.

Who this works well for:

- People saving for a goal that is one to five years away

- Anyone who does not need the money for anything urgent during that time

- People who want a simple, single institution solution

Where it falls short:

- CDs are not goal-specific. You deposit a lump sum, not ongoing contributions.

- The penalty is losing interest, not principal. If you really need the money, you can still get it.

- They are not designed for people making regular small contributions toward a specific named goal.

A CD ladder (opening multiple CDs at different maturities) can work well for long-term savers, but it adds complexity that many people do not want to manage.

Treasury Bills and I-Bonds {#treasury-bills-and-i-bonds}

Treasury Bills (T-Bills) are short-term US government debt instruments, typically maturing in four, eight, thirteen, twenty-six, or fifty-two weeks. You buy them at a discount and receive the full face value at maturity. Early sale is possible through the secondary market, but it adds friction and some potential loss.

I-Bonds are inflation-adjusted savings bonds issued by the US Treasury. They cannot be redeemed at all for the first twelve months, and if you redeem within five years, you lose three months of interest. After five years, they are fully liquid.

Who this works well for:

- People with a one-year-plus savings timeline

- Anyone concerned about inflation eating their savings

- People who benefit from a twelve-month hard lock (I-Bonds specifically)

Where it falls short:

- I-Bonds have a $10,000 annual purchase limit per person.

- The process of buying through TreasuryDirect.gov is clunky and not mobile-friendly.

- Neither product is built around naming a goal, tracking progress, or creating emotional connection to what you are saving for.

Employer Retirement Accounts {#employer-retirement-accounts}

A 401(k) or similar employer retirement plan is one of the most powerful forced savings mechanisms available. Contributions come out of your paycheck before you see them, and withdrawing before age 59½ triggers a 10% penalty plus income taxes on the withdrawn amount.

That combination, automatic contribution and steep early withdrawal penalty, is genuinely hard to defeat. Most people leave their 401(k) alone simply because touching it is so expensive.

Who this works well for:

- Anyone with access to an employer-sponsored plan, especially with a match

- Long-term retirement savers

- People who want money to disappear automatically with zero willpower required

Where it falls short:

- Retirement accounts are for retirement. Using them as a general savings lock for a vacation or emergency fund is not the intended use.

- The early withdrawal penalty is severe enough that this is not a practical tool for short or medium-term goals.

- Not everyone has access to one, especially freelancers and gig workers.

Goal-Based Locked Savings Apps {#goal-based-locked-savings-apps}

This is the category that has grown the most in recent years and is the most relevant for someone trying to save for a specific, named goal with regular contributions.

Goal-based savings apps let users set a target, contribute toward it over time, and, in the best versions, lock those contributions so they cannot easily be moved back into a checking account on a whim.

The key difference between a good locked savings app and a bad one is whether the lock has real teeth. A "goal" feature that lets you withdraw with no consequence is just a labeled bucket. A locked savings product that costs you real money to exit early is a commitment device.

There are a few broader options in this space worth knowing:

Long Game / Prize-Linked Savings Apps Some apps use prize drawings as motivation to keep money locked. You earn entries into drawings by saving rather than spending. The lock is lighter but the motivation model is different.

Credit Union Savings Certificates Many credit unions offer savings certificates (essentially CDs) with lower minimums and slightly better terms than big banks. The lock mechanism is still penalty-based interest loss.

Banking apps with "vaults" or "pockets" Apps like Monzo, Chime, and others offer labeled savings pockets. Some have withdrawal friction, but most do not have genuine financial penalties for early access. They help with organization, not commitment.

If you want a genuinely useful comparison of savings account types more broadly, the video below covers several options worth considering:

Bloomin: Locked Savings Built Around Consequences {#bloomin}

Bloomin is built specifically for people who keep spending their savings before they finish. It is not a budgeting app, a round-up app, or a bank. It is a commitment device that locks your savings toward a named goal and makes early withdrawal genuinely costly.

Here is how it works:

Step 1: Pick your goal before any money moves. Bloomin requires you to name what you are saving for before contributing a single dollar. Goal types include vacation, emergency fund, home, new baby, vehicle, education, celebration, and tech upgrade. The money has a job from day one.

Step 2: Contribute toward the goal. You add money from a saved payment method. Once that money is contributed, it is out of easy reach. There is no one-click transfer back to your checking account.

Step 3: Finish or pay to quit. This is the part that makes Bloomin different from most savings tools. When you reach your target, you unlock the money by paying a 1% finish fee. If you quit before reaching the goal, you lose 25% of your balance.

That 25% penalty is the real mechanism. It is not a mild inconvenience. It is a genuine consequence that makes most impulsive withdrawal decisions feel very different when you do the math. Walking away from $800 in savings costs $200. That is a real number.

Up to five goals at once. Bloomin keeps things focused by capping active goals at five. This prevents the "too many buckets" problem where savings get spread across so many goals that none of them feel real.

The rule stays visible. Every key screen in the app shows the finish fee and the early exit penalty. The consequence is not buried in a terms page. It is in front of you every time you open the app.

Who Bloomin is for:

- People who have failed repeatedly with regular savings accounts

- Anyone who needs the penalty to feel real rather than theoretical

- People saving for a specific, named goal over months

- Anyone who has tried budgeting apps and found that visible numbers do not stop them from spending

What Bloomin is not for:

- Emergency fund access where you might legitimately need the money fast (the 25% penalty would apply)

- Long-term retirement savings (that is what a 401k is for)

- People who already have strong savings discipline and just want a good interest rate

The honest tradeoff is that Bloomin's model works by making quitting expensive. For someone who genuinely keeps destroying their savings, that cost is worth it. For someone who just wants a slightly better savings structure, a high-yield savings account might be the simpler answer.

If you want to join the early access list, Bloomin has a waitlist open now.

How to Choose the Right Locked Savings Tool {#how-to-choose}

The right tool depends on three things: your timeline, your goal type, and how impulsive your spending habits actually are.

Timeline under one year: CDs with short terms, prize-linked savings apps, or a goal-based app like Bloomin all work here. Avoid I-Bonds (twelve-month minimum hold) and avoid retirement accounts entirely.

Timeline one to five years: CD ladders, I-Bonds (after the first year), or a locked savings app with automatic contributions are all worth considering. If the goal is specific, a goal-named app adds motivation that a CD does not.

Timeline over five years: Retirement accounts and I-Bonds are your strongest tools. The lock is real, the growth is compounding, and the forced savings mechanism is powerful.

If you are highly impulsive with savings: Choose the option with the steepest early withdrawal consequence you can tolerate. A CD's interest penalty might not be enough. A 25% balance penalty from Bloomin is harder to rationalize away. The goal is to make the consequence feel real before you contribute, not after.

If your goal needs a name and emotional connection: Generic savings tools fail here. When the goal is just a number in an account, it is easy to spend it without guilt. When the goal is labeled "vacation" or "home down payment," the emotional cost of raiding it is higher. Bloomin's named goal types are built around this insight.

For background on how different savings goals work and why goal clarity matters, the Bloomin post on the three types of saving goals explains the framework well.

Common Mistakes to Avoid {#common-mistakes}

People who struggle to keep their savings intact tend to make the same few mistakes when they try to fix the problem.

Mistake 1: Using a regular savings account and hoping this time will be different. It usually is not. The account has no friction, and the impulse wins again. The fix is structural, not motivational.

Mistake 2: Choosing a "locked" tool that is not actually locked. Banking apps with labeled pockets or savings goals that allow instant withdrawal are not locked savings products. They are organized savings. That is useful for different reasons, but it does not stop impulsive spending.

Mistake 3: Opening too many savings goals at once. When savings are spread across eight different goals with small balances in each, none of them feel significant. Progress is invisible. The temptation to consolidate everything into one spending account grows. Bloomin's five-goal cap exists for exactly this reason.

Mistake 4: Not reading the penalty structure before contributing. Every locked savings product has rules. CD early withdrawal penalties vary by institution. Bloomin's 25% exit penalty applies before the goal is reached. Knowing the cost ahead of time is how you make an informed commitment.

Mistake 5: Treating a locked savings tool as an emergency fund. Emergency funds need to be accessible. If you lock your emergency fund in a product with a steep early withdrawal penalty, you have created a new problem. Keep a small, separate accessible buffer for true emergencies, and use locked tools for goal-specific savings on top of that.

A Simple Checklist Before You Lock Your Savings {#checklist}

Before committing money to any locked savings product, run through this short checklist:

- [ ] Do you have at least a small accessible emergency buffer that is separate from this goal?

- [ ] Do you know your exact target amount?

- [ ] Do you know your target date, or at least an approximate timeline?

- [ ] Have you read the early withdrawal penalty for your chosen tool?

- [ ] Is the goal named and specific enough to feel real?

- [ ] Can you genuinely go without this money for the duration of the lock?

- [ ] Have you contributed an amount you can live without, not your entire savings?

If all of those boxes are checked, a locked savings product is likely the right move. If one or two are uncertain, resolve them before locking anything.

The Bloomin post on the 27-40 rule offers a useful framework for thinking about how to structure savings contributions if the question of how much to lock at once feels unclear.

Putting It All Together

There is no single best locked savings tool. The right answer depends on what the goal is, how long the timeline is, and how impulsive the saver tends to be.

For retirement and very long timelines, employer accounts with automatic contributions are hard to beat. For medium-term goals with lump-sum deposits, CDs and I-Bonds are solid. For short to medium-term, named, specific goals where someone has a history of raiding their savings, a purpose-built locked savings app with a real financial penalty is the most effective tool.

Bloomin is designed specifically for the last group. Not because discipline is impossible, but because removing easy exits works better than asking for more willpower. The finish fee is small (1%). The exit penalty is real (25%). The goals are named before the money moves. That combination is built to stop the cycle, not just comment on it.

If the pattern of saving and spending and starting over sounds familiar, it is worth exploring a tool designed for exactly that problem. You can join the Bloomin waitlist to get early access when it opens.

The savings goal is real. The next step is making it harder to undo.