blog

I Suck at Saving Money — Here Are Methods That Actually Work

If you keep spending your savings before reaching your goal, you're not alone. Here are real methods that remove temptation instead of demanding willpower.

I Suck at Saving Money: Here Are Methods That Actually Work

Here is the honest truth: if you keep dipping into your savings before you hit your goal, the problem probably is not your character. It is your setup.

Most savings advice tells you to try harder, want it more, or build better habits. That advice is not wrong exactly, but it skips the part where your brain is genuinely wired to prefer spending today over saving for later. Willpower is a limited resource. When the money is sitting in an account you can see and touch, you will eventually find a reason to move it.

The methods that actually work are not about wanting it more. They are about making it harder to access the money in the first place. Remove the exit, and you remove the temptation.

This post covers practical approaches, from the simplest mental reframes to the structural tools that put real friction between you and your savings.

Table of Contents

- Why most people fail at saving (it is not laziness)

- Method 1: Pay yourself first, automatically

- Method 2: Name your savings goals

- Method 3: Separate accounts for separate goals

- Method 4: Make the money hard to reach

- Method 5: Use commitment devices with real consequences

- Method 6: Set a savings cap you can actually live with

- Method 7: Track progress somewhere visible

- What to do if none of this has worked before

Why Most People Fail at Saving {#why-most-people-fail}

It helps to understand what is actually happening before trying to fix it.

When money sits in a regular savings account tied to your checking account, it is one transfer away. One bad week, one sale, one unexpected dinner, and it is gone. You did not fail because you are irresponsible. You failed because the path of least resistance was to spend it.

Behavioral economists call this present bias: humans consistently overvalue what they can have right now compared to what they could have later. A vacation six months from now feels abstract. A pair of shoes today feels very real.

This is also why budgets fail so often. A budget is a plan. Plans require constant decision-making. Every time money sits available in an account, your brain has to make a new decision about whether to spend it. Decisions are exhausting, and eventually the answer becomes yes.

The goal of every method below is to reduce how many decisions you have to make, or to make the wrong decision painful enough that you stop before you act.

Method 1: Pay Yourself First, Automatically {#pay-yourself-first}

This is the foundational move. Instead of saving whatever is left over at the end of the month, you move money to savings the moment you get paid, before it ever sits in your spending account.

The psychology is simple: you can only spend what you can see. If the money never shows up in your main account, you adjust your spending to whatever is left.

Most banks and employers let you split direct deposit between accounts. Set it up once and it runs without you. If your employer does not support split deposit, schedule an automatic transfer for the day after payday.

The amount matters less than the habit. Starting with 5% of each paycheck is better than promising yourself 20% and never doing it.

Method 2: Name Your Savings Goals {#name-your-goals}

A savings account labeled "savings" is boring. A savings account labeled "Japan trip - May 2026" is a story you are telling yourself about the future.

Naming your goals changes how you relate to the money. When you think about pulling from it, you are not withdrawing from an abstract number. You are stealing from your vacation.

Research in behavioral finance consistently shows that people save more and dip into savings less when money has a specific mental label attached to it. This is sometimes called "mental accounting." You use it against yourself all the time when you justify spending because "it's fun money." You can use it in your favor too.

Before you set up any savings bucket, decide exactly what the money is for. Not "emergency fund" in a vague sense, but "three months of rent if I lose my job." Not "home stuff" but "down payment on a place before my lease ends."

Check out what are the three types of saving goals if you want a clear breakdown of how to think about goal types before you start building buckets.

Method 3: Separate Accounts for Separate Goals {#separate-accounts}

Once your goals are named, keep them in physically separate places.

A single savings account for multiple goals is a mess. When you need to pull from "vacation," you might accidentally drain the emergency fund too, because it all looks like one pile of money.

Here is a simple setup:

- Checking account: money for bills and daily spending

- Emergency fund account: separate bank, low interest is fine, just keep it separate

- Goal-specific accounts: one account per major goal if possible

Yes, this means managing a few more accounts. But most modern banks let you open sub-accounts or savings pockets for free. The friction of having to go to a different account, log in, and transfer is enough to stop a lot of impulse withdrawals.

Some people go further and use a different bank entirely for long-term savings. The extra step of moving money back takes a few days with a bank transfer, which is enough cooling-off time to talk yourself out of a bad decision.

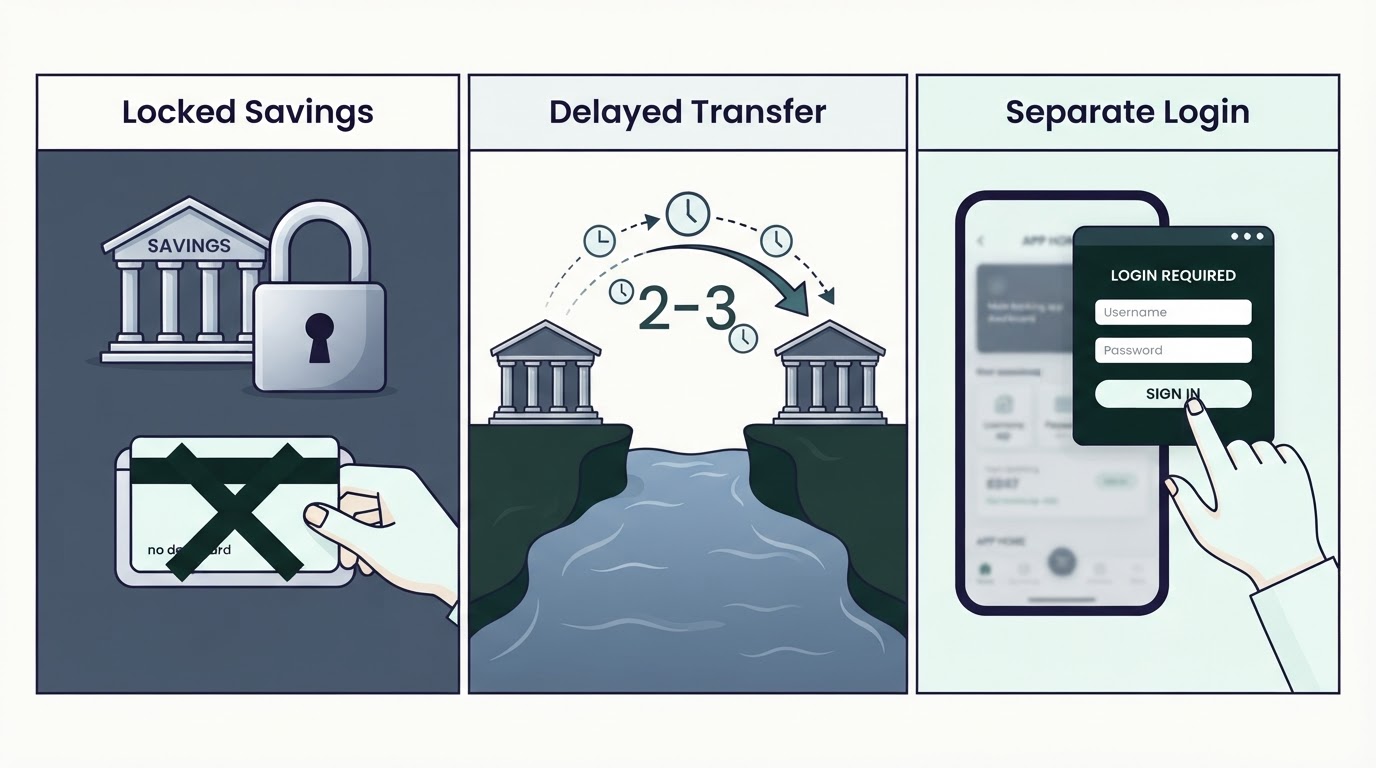

Method 4: Make the Money Hard to Reach {#make-it-hard-to-reach}

The harder it is to access, the more likely you are to leave it alone. This sounds obvious, but most savings setups are designed for easy access, which works against you.

Some ways to add friction:

No debit card attached. Open a savings account without requesting a debit card. If you cannot tap to pay, you have to make a deliberate effort to move money out.

Use a different bank than your checking. As mentioned above, ACH transfers between banks take one to three business days. That delay is your friend.

Remove the account from your main banking app. Out of sight helps. If you have to log into a separate app to see the balance, you will check it less, which means you will be tempted less.

Certificates of deposit (CDs). A CD locks your money for a set period, usually three months to five years. Withdrawing early usually costs a penalty of several months of interest. Not ideal for everyone, but effective if you know you will not need the money soon.

The theme here is deliberate friction. You are not relying on willpower. You are engineering an obstacle course between yourself and the money.

Method 5: Use Commitment Devices with Real Consequences {#commitment-devices}

A commitment device is when you voluntarily give up some freedom now to protect a future outcome. Think of it as making a promise to yourself with teeth.

The classic example is Ulysses ordering his sailors to tie him to the mast before sailing past the Sirens. He knew he would want to jump. So he made jumping impossible before the temptation arrived.

You can do this with money in a few ways:

Savings challenges. The 52-week challenge, where you save $1 in week one, $2 in week two, and so on, works partly because you feel a social and personal commitment to not break the streak. Many people do these publicly with a partner or in a group to add accountability.

Savings apps with penalties. Some apps are specifically built around commitment. Bloomin is one example. You pick a goal, lock money toward it, and the terms are clear up front: finish your goal and pay a small 1% unlock fee, or quit early and lose 25% of your balance. That penalty changes the math on impulse withdrawals completely. It is not just "I'm taking money from my future self." It is "I am about to lose a quarter of what I saved."

This kind of consequence is the point. Willpower is unreliable. Consequences are not.

If you want to understand more about why touching savings feels so hard to resist, how to stop touching your savings goes deeper into the psychology and what actually works.

Method 6: Set a Savings Cap You Can Actually Live With {#savings-cap}

One of the most common reasons people raid their savings is because they saved too aggressively and left themselves too little to spend.

If your monthly budget is too tight after the savings transfer, you will resent the savings. At some point you will crack, pull from it, and feel guilty. Then you will repeat the cycle.

The fix is not to save less forever. The fix is to start with a number that does not hurt.

If saving $500 a month makes your checking account feel empty and stressful, try $200. A smaller amount consistently kept is worth more than a large amount that gets raided every other month.

There is a useful framework called the 27/40 rule that helps figure out what percentage of income to allocate to savings based on your situation. What is the 27/40 rule explains how it works if you want a starting point that is less arbitrary than picking a number out of thin air.

The goal is to find a number that your brain accepts as "already spent" the moment you get paid. Once saving feels like a fixed expense, not a choice you are making every month, the money is much safer.

Method 7: Track Progress Somewhere Visible {#track-progress}

Progress tracking sounds like a minor detail but it actually shifts your relationship with saving.

When you can see that you are 43% of the way to a vacation fund, the mental shift is real. You are no longer "someone who is trying to save." You are "someone who is almost halfway there." The money in that account stops feeling like money and starts feeling like progress toward something specific.

A few ways to track:

A physical savings tracker. Print a simple chart and color it in each time you contribute. Sounds silly, works well. The physical act of marking progress gives a small dopamine hit.

A shared spreadsheet. If you have a partner or savings buddy, keeping a shared log adds light accountability without making it heavy.

An app that shows goal progress. Many savings apps show a percentage or a progress bar. That visual cue matters more than people expect. Apps like Bloomin are built around making progress visible on every screen, so you always know exactly where you stand on each goal.

A sticky note on your laptop or mirror. A dollar amount with a checkmark for each contribution. Low tech, high visibility.

Whatever method you use, the key is that it should be easy to update and satisfying to look at. If tracking feels like homework, you will stop doing it.

A Note on Focusing on Too Many Goals at Once

Here is a pattern worth watching for: spreading your savings across too many goals at once, so none of them feel like they are going anywhere.

If you are trying to save for an emergency fund, a vacation, a car repair, a new laptop, and a wedding gift all at the same time, each goal gets such a small contribution that progress is invisible. Invisible progress kills motivation.

Bloomin caps users at five active goals for exactly this reason. It is easy to open ten saving buckets and feel organized while never actually finishing any of them. The cap forces you to prioritize, which makes each goal feel more real and more finishable.

A good rule: no more than three active savings goals at any time. Rank them by urgency and work from the top. When one is done, add the next one.

What If You Are Starting from Zero?

Starting from a savings balance of zero feels overwhelming, especially if you have already tried and failed a few times.

Here is a realistic starting point:

Step one: Open a separate savings account with a different bank than your checking account. Do this today, even if you put nothing in it yet.

Step two: Set up a $25 automatic transfer on payday. Not $200, not $500. Twenty-five dollars. Let it run for a month without touching it.

Step three: Name the account something specific. "Car repair fund" or "vacation 2026." Anything that is not just "savings."

Step four: After one month, look at the balance. You now have $25 to $50 in there. That is real money that was not there before. Now decide if you can increase the transfer to $50.

Step five: Once you have a small foundation, look at adding a penalty-based structure if you know you will be tempted. That is where apps like Bloomin are useful, because the penalty makes the cost of quitting visible before you ever put money in.

The reason to start this small is not because $25 is impressive. It is because you need to prove to yourself that you can leave money alone. One month of leaving $25 untouched is worth more psychologically than a big savings push that gets raided two weeks in.

What to Do If None of This Has Worked Before {#if-nothing-has-worked}

If you have tried separate accounts, automation, goal naming, and budgeting apps, and still found a way to raid the money, the honest next step is to look at commitment devices with hard consequences.

Soft friction (separate accounts, tracking apps, goal names) helps most people. But some people need a harder wall.

The tools that work for this group share one feature: getting the money back hurts. Whether that is a CD with an early withdrawal penalty, or an app that takes 25% of your balance if you quit early, the consequence has to feel real.

That is the entire premise behind Bloomin. The app is not a budgeting tool or a tracker. It is a commitment device. The lock is the product. You put money in, it stays in, and the cost of getting it out before you finish is high enough to make you think twice, three times, and then probably just leave it alone.

Some people feel nervous about penalty-based savings. That is reasonable. But think about what "losing 25%" actually means in practice. If you save $1,000 toward a vacation and quit early, you lose $250. That stings. Now compare it to the alternative: you slowly drain the $1,000 over three months and end up with nothing and no vacation. Which outcome is worse?

The penalty is a feature, not a punishment. It is the thing that makes the commitment real.

Quick Reference: Methods at a Glance

| Method | What It Does | Best For |

|---|---|---|

| Pay yourself first | Removes money before you can spend it | Everyone, start here |

| Name your goals | Adds identity and meaning to each bucket | People who feel abstract about savings |

| Separate accounts | Creates physical distance from spending money | People who move money impulsively |

| Hard-to-reach accounts | Adds time delay to withdrawals | Impulse spenders |

| Commitment devices | Makes quitting expensive | People who have tried everything else |

| Realistic savings cap | Prevents resentment and raiding | People who set and break big targets |

| Progress tracking | Builds motivation and momentum | People who lose interest mid-goal |

The Bottom Line

Saving is not mostly a discipline problem. It is mostly a structure problem. Most people who struggle to save are not bad with money. They just have their money sitting somewhere too easy to reach.

The methods that work longest are the ones that take willpower out of the equation. Automate the transfer. Name the goal. Separate the account. Add friction. And if you need it, add a real consequence for quitting early.

None of this requires you to become a different person. It requires you to set up your accounts and tools in a way that accounts for the person you already are: someone who will spend money if it is easy to reach, and someone who will leave it alone if getting to it is annoying enough.

If you want to try the penalty-based approach and see if a hard lock is what finally makes saving stick, join the Bloomin waitlist and get early access when the app opens. It was built specifically for people who know they need more than a tracker.