blog

Summer Fun Shouldn't Come at the Expense of Your Savings

Summer costs add up fast and savings disappear just as quickly. Here's how to enjoy the season without blowing your financial goals.

Summer Fun Shouldn't Come at the Expense of Your Savings

Summer has a way of making spending feel completely justified. It's warm, everyone's making plans, and there's a collective feeling that now is the time to live a little. Road trips, concerts, beach weekends, backyard parties, flights to see family, kids' activities when school is out. The list grows fast, and so does the tab.

The problem isn't that people want to enjoy summer. The problem is that summer spending often pulls directly from money that was already earmarked for something else. The vacation fund quietly becomes the "everything fund." The emergency savings gets raided for a last-minute trip. By September, the balance looks nothing like it did in May, and the goals that felt so solid in January are back to square one.

Summer fun is real and worth protecting. So are savings goals. The good news is that both can coexist, and it doesn't require being miserable all season to make it happen.

What's In This Post

- Why summer reliably wrecks savings

- The psychology behind seasonal overspending

- How to plan a summer budget without ruining the fun

- What happens when savings aren't protected from impulse

- How locked savings goals change the game

- Practical ways to enjoy summer on a real budget

Why Summer Reliably Wrecks Savings

It's not random. Summer spending follows a predictable pattern, and understanding it makes it easier to get ahead of.

First, summer is full of social pressure. People are more visible in the summer. Plans get posted, invitations pile up, and saying no can feel like opting out of life. Spending becomes tied to belonging, to being present for the people around you.

Second, summer has a "treat yourself" atmosphere that doesn't exist in quite the same way in February. The season itself feels like a reward. That feeling makes it much easier to rationalize purchases that wouldn't fly in October.

Third, summer surprises compound quickly. One weekend trip becomes two. One festival becomes a habit. The kids need camp, then supplies, then new gear for back-to-school before you've had time to recover from Memorial Day.

None of this is a character flaw. It's just how summer works financially for most people. The spending is real, the joy is real, and the damage to savings goals is also real.

The Psychology Behind Seasonal Overspending

There's a well-documented gap between what people intend to do and what they actually do with money. Psychologists sometimes call this the intention-action gap. People mean to save more, spend less, and stick to their plans, and then life happens.

Summer intensifies this gap for a few reasons.

Present bias. The human brain is wired to value the present more than the future. A beach trip this weekend feels more real than a down payment two years from now. When a fun opportunity sits right in front of someone, the savings goal in an app feels abstract by comparison.

Availability of funds. Most savings accounts are just a transfer away. There's no barrier between the savings and the checking account. When money is easy to access, it gets accessed. This is not a willpower problem. It's a friction problem.

Normalizing creep. One small splurge feels fine. Then another. Then it feels normal to spend a little extra during summer. By August, the pattern is cemented and the savings are gone.

This is worth naming clearly: the issue isn't that people don't care about their goals. It's that the system they're using makes it too easy to undermine those goals in moments of impulse.

How to Plan a Summer Budget Without Ruining the Fun

Budgeting for summer doesn't mean refusing every invitation or staying home all season. It means deciding in advance what gets money and what doesn't, so there's no guilt and no regret at the end of August.

Step 1: Name the things that actually matter

Not every summer expense brings the same amount of joy. A family reunion trip might matter a lot. Weekly takeout because it's hot and nobody wants to cook might matter less. Thinking through which summer experiences are actually worth the spend gives a cleaner picture of where money should go.

This is a good time to read about what are the three types of saving goals, because not all savings goals are equal. Some are urgent, some are meaningful, and some are more aspirational. Knowing the difference helps prioritize what summer spending is actually worth disrupting.

Step 2: Assign a number to summer

A summer budget doesn't need to be complicated. It can be a single number: "We're spending X on summer this year." That number covers everything, from weekend plans to spontaneous ice cream runs. Once the number exists, every decision is easier because the context is already set.

Without a number, every expense gets evaluated in isolation, which makes it easy to justify each one individually while the total creeps out of control.

Step 3: Separate summer spending from savings goals

This is the most important step. Summer fun money and savings goal money should not live in the same place.

If vacation savings are sitting in a general checking account or even a regular savings account with easy transfers, they will get blended into summer spending. The solution is separation, ideally physical separation where the savings are harder to reach.

Step 4: Protect the savings before summer starts

Move savings goal money somewhere it can't be easily touched before summer begins. This isn't about hiding money from yourself. It's about removing the easy path so that the harder path, which requires intention, becomes the only option.

This is where tools that create real friction start to matter more than good intentions.

What Happens When Savings Aren't Protected

Here's a scenario that plays out for a lot of people every summer.

Someone starts May with $1,800 saved toward a vacation fund. The goal is $3,000 by October for a trip that's been on the wish list for two years. They're excited. The progress feels real.

Then summer arrives. A friend's bachelorette trip comes up, around $300. A weekend at the lake needs a hotel, another $180. The kids need summer camp supplies. There's a concert, a birthday dinner, a spontaneous road trip to see family. Each expense feels reasonable in isolation. Most of them are genuinely fun.

By August, the vacation fund is at $900. The October trip is no longer happening. And because the money is already gone, starting over feels pointless, so the goal gets shelved entirely.

This is the pattern that repeats every year for people who keep savings accessible. The goal doesn't fail because the person stopped caring. It fails because there was no barrier between the goal money and the summer spending.

If you recognize this pattern in yourself, how to stop touching your savings is worth reading carefully. It gets into the specific mechanics of why accessible savings are always at risk.

How Locked Savings Goals Change the Game

Willpower is not a reliable savings strategy. It works sometimes, in the right mood, when life isn't throwing curveballs. But it doesn't work consistently, and summer is not exactly a low-temptation season.

What actually works is structure. Specifically, a structure where taking money out of a goal requires a cost, not just a click.

This is the idea behind commitment devices. A commitment device is any system that binds a future choice so that a person's present self can't easily undo what their future self committed to. Think of it as making a deal with yourself that has actual consequences.

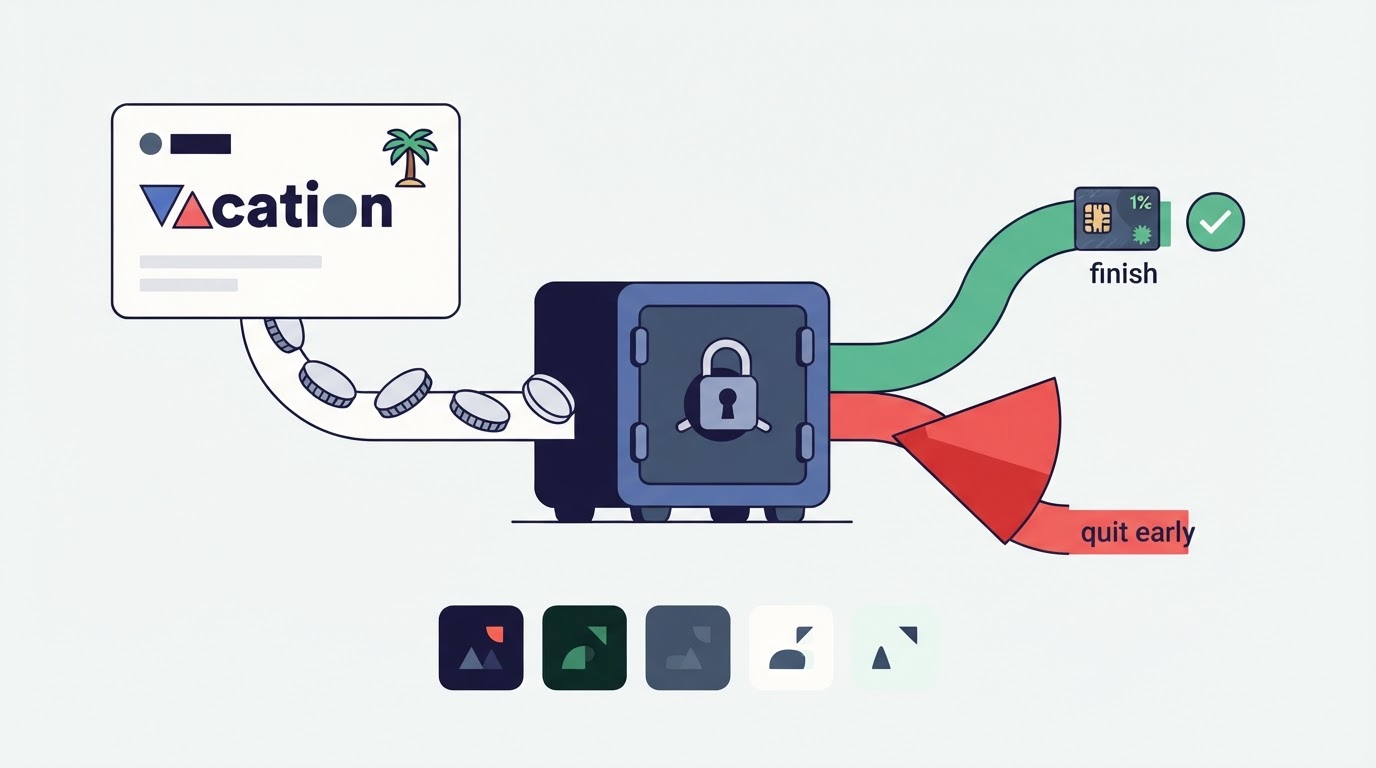

Apps like Bloomin are built around this idea. Instead of a regular savings account that anyone can drain in seconds, Bloomin locks contributions toward a named goal. To get the money out before the goal is complete, the user pays a 25% penalty. That consequence exists on purpose. It's the barrier between a moment of impulse and a savings goal that actually reaches the finish line.

The way it works:

- A user picks a specific goal, such as vacation, emergency fund, home, vehicle, or education.

- They contribute money toward that goal.

- The money locks. It's not accessible with a quick transfer.

- If they finish the goal, they pay a 1% fee to unlock the funds.

- If they quit early, they lose 25% of the balance.

The consequence is visible before any money moves. Users know exactly what walking away will cost, and that knowledge changes behavior in a way that a note in a journal or a goal in a regular savings app simply doesn't.

The fee structure deserves a closer look because it's not punitive for its own sake. The 1% finish fee for completing a goal is genuinely small. On $3,000 saved, that's $30. On $5,000, it's $50. That's a very reasonable cost for the structure and accountability that came with it. The 25% early-quit penalty is steep by design, because the whole point is to make quitting feel real. A small penalty is easy to shrug off. A 25% penalty is not.

Bloomin also limits users to five active goals at a time. This is a feature, not a limitation. Spreading savings across too many goals dilutes progress and makes it easy to treat every category as optional. Five focused goals keeps priorities clear.

Practical Ways to Enjoy Summer on a Real Budget

Protecting savings doesn't mean skipping summer. It means being intentional about how summer spending happens, so that there's money for what matters without destroying goals in the process.

Have the summer "fun money" conversation early

If partners, roommates, or families are involved, getting aligned before summer starts saves a lot of friction later. What's the household summer budget? What trips or events are non-negotiable? What's fair game to skip? These conversations feel awkward but they prevent the much more awkward September conversation about why the savings are gone.

Look for free and low-cost summer experiences

Summer has more genuinely free activities than any other season. Outdoor concerts, hiking, beach days, farmers markets, community events, backyard hosting. None of these require much spending, and most of them are actually better than expensive alternatives because they're unhurried.

This isn't about deprivation. It's about filling the summer with things that are genuinely enjoyable rather than expensive by default.

Use the 48-hour rule for unplanned summer spending

When an unplanned expense comes up, waiting 48 hours before committing filters out a meaningful portion of impulse purchases. Summer is full of spontaneous invitations and limited-time opportunities. Some of them are worth it. Many of them feel less compelling two days later.

The 48-hour rule doesn't require saying no to anything. It just requires saying "let me think about it" before the credit card comes out.

Lock the savings goal before summer starts, not after

This is timing that matters. Locking a savings goal in April, before summer spending pressure picks up, is far more effective than trying to protect savings in July when the pressure is already at its peak.

If the goal money is already locked somewhere that has real exit friction, it never becomes "available" during summer in the first place. It stays separate from the fun money, does its job quietly in the background, and arrives at the finish line intact.

Track summer spending without obsessing over it

A simple check-in every two weeks works better for most people than a daily tracking ritual that burns out by week three. The goal is awareness, not anxiety. Knowing roughly where summer spending stands every couple of weeks makes it easy to course-correct before things go sideways.

The Real Cost of Spending Savings in Summer

It's easy to treat a drained savings goal as a setback that can be recovered quickly. In practice, the cost is often higher than it looks.

There's the obvious financial cost. If someone saved $2,000 over six months and spends it in summer, they're not just back to zero. They've used six months of momentum and have to start over from scratch, often with less motivation the second time.

There's also the compounding cost. Money that stays invested or in a dedicated savings account grows. Money that gets spent on a summer weekend does not. The difference between finishing a goal on time and starting over after summer is often measured in months, sometimes years.

And there's the psychological cost. People who repeatedly blow through their savings goals before reaching them often internalize it as a personal failure. They start to believe they're just bad at saving, which makes it harder to try again. This is the most expensive outcome because it isn't just about one goal. It poisons future attempts.

Understanding this pattern is why tools like Bloomin exist. Not to punish spending, but to protect the follow-through that most people genuinely want but keep undermining with easy access to their own money.

If you're curious about saving structures that actually account for human behavior, the 27/40 rule is a useful framework for thinking about how savings fit into the bigger picture of a monthly budget.

Saving for Summer vs. Saving Through Summer

There are actually two different savings challenges here, and they're worth naming separately.

Saving for summer means setting money aside in advance specifically to fund summer activities. This is the smart move. Instead of spending from savings that were meant for something else, a person builds a dedicated "summer fund" that exists for exactly this purpose. When summer arrives, the fund gets used as designed, and the other savings goals stay untouched.

Saving through summer means keeping a longer-term goal on track even while summer spending happens around it. This is harder because the temptation to borrow from the goal is at its highest. It requires the savings to be in a place where borrowing isn't easy.

Both strategies benefit from the same core principle: separate the money and make access harder than a quick app transfer.

Setting Up a Summer That Doesn't Require a Choice Between Fun and Goals

The practical setup is simpler than most people expect.

Before summer starts, do three things.

First, decide how much is fair to spend on summer fun. Write it down somewhere visible. This is the summer budget.

Second, lock all current savings goals in a place that has real friction. If using Bloomin, the money goes into a named goal and stays there until either the goal is complete (paying the 1% finish fee) or the user decides the 25% penalty is worth it. In most cases, that penalty is enough to keep the money right where it belongs.

Third, open a separate account or portion of spending money specifically labeled for summer. This is the fun money. When it's gone, summer fun scales back. The savings goals never come into contact with this decision.

That's the whole system. Three steps, done before June, and summer can actually be enjoyed without the financial hangover in September.

What the End of Summer Should Look Like

The goal is to reach September with the savings goals still intact, a summer full of real memories, and none of the regret that comes from realizing the goals were quietly gutted over three months.

That outcome is achievable. It doesn't require austerity or perfect discipline or skipping the things that actually matter. It requires a plan, a budget, and savings that are genuinely protected from impulse.

Summer fun is worth every penny when it's budgeted for. The trips, the weekends, the concerts, the spontaneous moments, all of it lands differently when there's no guilt attached and no savings goal quietly suffering in the background.

Ready to Protect Your Savings This Summer?

If the pattern of spending savings before reaching a goal sounds familiar, the structure might matter more than the intention at this point. Bloomin is built for exactly this situation: people who want to hit their goals but keep getting in their own way.

The app locks contributions toward a named goal, keeps the consequences visible, and removes the easy exit that makes summer such a reliable threat to savings. Users who finish their goal pay 1% to unlock. Users who quit early lose 25%. That's not a punishment. That's a commitment device that actually works.

If Bloomin sounds like the kind of friction you've been looking for, join the waitlist and get your spot in the first invite wave.

Summer is long. Savings goals are longer. Both deserve to finish intact.