blog

Top Mistakes People Make When Saving Money (And How to Actually Fix Them)

Most people don't fail at saving because they're careless. They fail because of small, fixable mistakes. Here's what those are and how to stop them.

Top Mistakes People Make When Saving Money (And How to Actually Fix Them)

Most people who struggle to save money are not bad with money. They're just repeating a handful of small, fixable mistakes without realizing it.

The problem is not usually income. It's not willpower either, at least not in the way most people assume. The real issue is that saving money requires a system, and most people never build one. They rely on whatever's left over at the end of the month, assume good intentions will carry them through, and then wonder why their savings account looks the same three months later.

This post breaks down the most common savings mistakes in plain terms, explains why each one actually hurts, and gives concrete ways to fix them.

Table of Contents

- Saving whatever is left instead of saving first

- Not having a specific goal

- Keeping savings too accessible

- Trying to save for too many things at once

- Treating savings like a backup spending account

- Ignoring small recurring expenses

- Saving without any timeline

- Waiting for the "right time" to start

- Relying entirely on motivation

- Not building in any friction

Saving Whatever Is Left Instead of Saving First {#saving-whatever-is-left}

This is probably the most universal mistake, and it kills more savings goals than anything else.

The logic feels reasonable: spend what needs to be spent, and then save whatever remains. But in practice, there is almost never anything left. Life fills the gap. Dinners, subscriptions, an impulse purchase, a friend's birthday gift. By the end of the month, the balance is basically the same.

The fix is simple in concept but requires a small shift in how the brain frames money. Save the amount first, before anything else gets spent. Treat the savings contribution like a bill, something that gets paid on payday, not something that happens if conditions are favorable.

This is sometimes called "paying yourself first." When the savings happen at the top of the month automatically, the rest of the month adjusts around it. When savings happen at the bottom, they usually don't happen at all.

Even starting with a small amount, say $50 or $100 per paycheck, and automating it immediately builds a habit that scales. The size matters less than the consistency and the timing.

Not Having a Specific Goal {#not-having-a-specific-goal}

Saving money "in general" doesn't work. It sounds responsible, but vague intentions don't survive contact with a real temptation.

When there is no specific goal attached to the money, it is easy to justify pulling from it. It's just sitting there. What's the harm in using a little now and replacing it later?

A specific goal changes that mental accounting entirely. When someone is saving for a vacation to Portugal in October, that money has a job. Spending it on something else isn't just a minor setback, it's directly delaying the thing they actually want.

This is why naming a goal matters. It's not just motivational. It creates a psychological ownership around the money that makes it harder to justify raiding.

If you want to understand the different types of savings goals and how they work, this breakdown of the three types of saving goals is worth reading before you decide where to start.

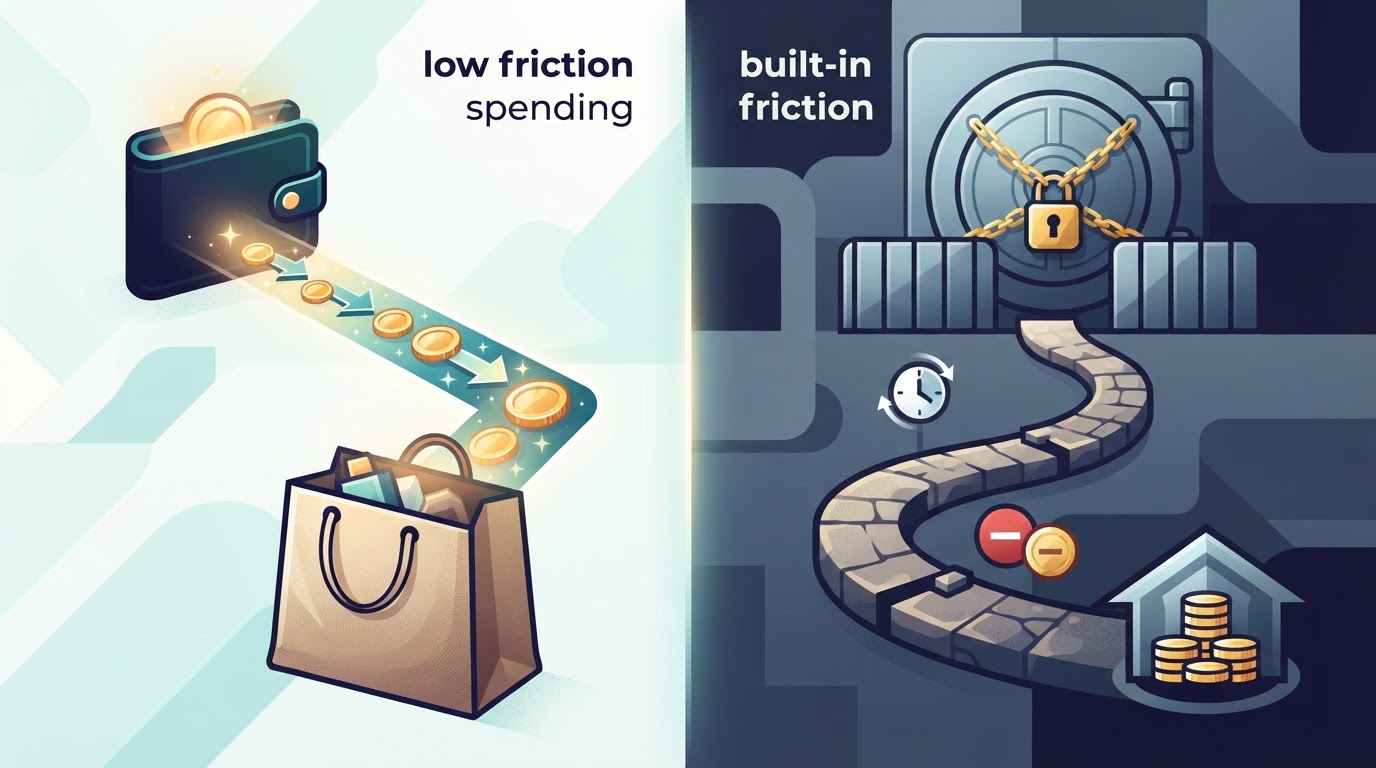

Keeping Savings Too Accessible {#keeping-savings-too-accessible}

Convenience is the enemy of savings.

When savings live in the same bank account as spending money, or even in a linked savings account that takes 30 seconds to transfer from, the friction to access it is essentially zero. And when friction is zero, impulse wins.

This isn't a character flaw. It's just how the human brain works. When something is easy, we do it. When something requires effort, we pause. That pause is often enough to stop a bad decision.

The research on this is well-established. Behavioral economists call it "friction," and it's one of the most reliable ways to change behavior without relying on willpower. Adding a delay, a penalty, or an extra step between a person and their savings dramatically reduces the chance they'll access it impulsively.

There are a few ways to increase that friction. One is using a bank account at a separate institution with no debit card attached, which means a transfer takes a couple of days. Another is using a goal-specific locked savings structure where the money physically cannot be accessed without a consequence.

The goal is not to make the money impossible to reach, but to make reaching it feel like a real decision rather than a reflex.

Trying to Save for Too Many Things at Once {#saving-for-too-many-things-at-once}

Having eight active savings goals sounds organized. In practice, it usually means none of them move fast enough to feel meaningful, and the whole system falls apart within a few weeks.

When someone splits $300 across eight goals, each one gets $37.50 per month. At that pace, a $3,000 vacation fund would take almost seven years. The slowness is demoralizing. Progress that is invisible doesn't feel like progress, and people stop contributing.

Limiting active goals forces prioritization. It makes people choose what actually matters right now versus what sounds good in the abstract. Fewer goals, funded more aggressively, reach the finish line faster. Reaching a goal feels good and builds momentum for the next one.

This is one of the more counterintuitive points about savings systems. Less choice leads to more output.

Treating Savings Like a Backup Spending Account {#savings-as-backup-spending}

This is related to accessibility but it deserves its own section because the behavior is so specific.

Some people have no trouble putting money into savings. Their problem is that they take it back out just as easily. They contribute $400 to the vacation fund, then borrow $200 from it when a concert comes up, then borrow another $150 when the car needs work. The goal never moves.

This pattern is incredibly common, and the frustrating part is that the person is doing the right thing by saving in the first place. The failure point isn't their values. It's their access to what they've saved.

The solution isn't willpower. The solution is making the money harder to touch. Whether that's a separate institution, a certificate of deposit with an early withdrawal penalty, or a purpose-built app that locks the balance, the mechanism matters more than the intention.

For people who recognize this pattern in themselves, this piece on how to stop touching your savings goes into more depth on why it happens and what actually helps.

Ignoring Small Recurring Expenses {#ignoring-small-recurring-expenses}

This one sneaks up on almost everyone.

Small recurring charges are invisible in a way that large purchases are not. A $14.99 streaming service, a $9.99 app subscription, a $12 monthly fee for something barely used, none of these feel significant on their own. But five or six of them together add up to $70 to $100 per month. Over a year, that's close to $1,000 that could have been saved.

The problem is not that these expenses are unreasonable. Some of them are worth every dollar. The problem is that most people aren't actually tracking them, so they don't know which ones they're using and which ones are just quietly draining the account.

A yearly audit of recurring charges, even a quick 20-minute pass through bank statements, almost always surfaces at least one or two subscriptions that can be cancelled immediately with no real loss to daily life.

That money, redirected automatically into a savings goal, compounds quickly.

Saving Without Any Timeline {#saving-without-a-timeline}

A goal without a deadline is just a wish.

When there's no target date attached to a savings goal, there's no urgency. It can always be started more seriously next month. The lack of a timeline removes any pressure to take consistent action now.

A timeline does a few useful things. First, it tells you exactly how much to save per month to hit the goal on time. Second, it creates a real sense of momentum or urgency as the date approaches. Third, it forces an honest conversation about whether the goal is achievable, which often leads to adjustments in timeline, contribution size, or scope.

For example, saving $5,000 for a home repair fund without a date attached is very different from saving $5,000 by January with a monthly contribution calculated and scheduled. The second version has a plan. The first one is a vague aspiration.

Pairing a named goal with a specific date is one of the lowest-effort, highest-impact changes a person can make to their savings habit.

Waiting for the "Right Time" to Start {#waiting-for-the-right-time}

The right time is not coming.

There will always be a reason to wait: the upcoming expense, the slightly unstable income month, the project at work that's eating all mental bandwidth. These reasons feel legitimate in the moment. But they have a way of cycling through repeatedly, and the person who waits for clear conditions before starting often never starts.

The more honest version of "I'll start saving when things settle down" is usually "I don't have a system that makes saving feel manageable right now."

Starting small solves most of this. $25 a week is not an impressive savings rate. But it builds the habit, proves the system works, and creates something to build on when more money is available. The goal of starting small is not to stay small. It's to create the infrastructure so that scaling up is easy.

Waiting for conditions to be perfect before beginning is one of the most expensive financial decisions most people make without realizing it's a decision at all.

Relying Entirely on Motivation {#relying-entirely-on-motivation}

Motivation is not a savings strategy.

People feel motivated to save after a scary bank statement, a financial article that hits close to home, or a conversation with someone who just paid off their debt. That motivation can be real and powerful. But it fades. Life gets busy. The urgency fades. The savings behavior stops.

Motivation is a starting point, not a long-term mechanism. What keeps a savings habit going after the motivation fades is structure, automation, and accountability.

Automation handles the consistency problem. When contributions happen automatically on a schedule, they don't require any motivation at all. The decision gets made once, and the system runs itself.

Accountability changes the cost calculation. When there are real consequences for breaking a commitment, the temptation to quit is no longer just a matter of how motivated someone feels. There is actual friction, an actual cost, an actual reason to stay the course even on a bad day.

Designing a system that works when motivation is low is far more valuable than trying to sustain high motivation indefinitely.

Not Building In Any Friction {#not-building-in-friction}

This is the mistake underneath many of the other mistakes on this list.

When money is easy to move, it will be moved. When a savings goal has no protective layer around it, every stressful week or tempting purchase becomes a genuine threat to the balance.

Friction is not punishment. It's architecture. It's the difference between a door with a lock and a door you just have to push open.

A few ways to build real friction into a savings system:

Separate institutions. Moving money from one bank to another takes one to three business days. That delay is often enough to let the impulse pass.

Certificates of deposit. CDs lock money for a set term with an early withdrawal penalty. The penalty creates a real cost for accessing money early.

Savings apps with lock mechanics. Tools that specifically prevent easy access to contributed money add a structural layer that regular bank accounts simply don't have.

Named goals. Assigning a purpose to each saved dollar makes it psychologically harder to redirect. The money isn't just savings. It's the vacation. It's the emergency fund. It's the new laptop.

Real consequences. Some systems go further and attach a penalty to early withdrawal. When someone knows that accessing the money early will cost them a percentage of what they saved, the calculation changes.

This last point is worth dwelling on. People often think they need more motivation or more discipline. What they usually need is a reason not to quit that exists independently of how they feel on any given day.

Why Willpower Alone Doesn't Work

There's a common assumption woven through most savings advice: that success is a matter of character. If someone can't save, they're undisciplined. If someone keeps spending their savings, they lack self-control.

This framing is not useful and it is not accurate.

Research in behavioral economics has shown consistently that people make worse decisions when they're tired, stressed, or overwhelmed, which is exactly when financial temptation tends to hit hardest. Expecting willpower to hold under those conditions is not realistic.

The smarter approach is designing a system that doesn't require willpower to function. Automation removes the need to make a decision each month. Locking mechanisms remove the ability to undo the decision without a cost. Named goals keep the reason visible. A timeline creates urgency.

None of these require the person to be more disciplined. They just make the right behavior easier and the wrong behavior harder.

If you're curious about structured saving approaches, the 27/40 rule offers a useful framework worth understanding alongside the ideas in this post.

A Quick Look at How These Mistakes Stack Up

Here's a practical summary of the most common mistakes and the fix for each one:

| Mistake | Why It Hurts | The Fix |

|---|---|---|

| Saving what's left over | Nothing is ever left | Pay yourself first, automatically |

| No specific goal | Easy to raid the money | Name the goal before moving money |

| Too-accessible savings | Zero friction to spend it | Add distance or lock mechanisms |

| Too many goals at once | None of them move | Limit to a focused few |

| Using savings as backup spending | Balance never grows | Separate and restrict access |

| Ignoring subscriptions | Silent monthly drain | Annual audit and cancellation |

| No timeline | No urgency or plan | Attach a target date |

| Waiting for the right time | Never starts | Begin small, adjust later |

| Relying on motivation | Fades quickly | Automate, don't rely on feeling |

| No friction built in | Impulse wins too easily | Lock it, delay it, cost it |

The Argument for a Commitment Device

A commitment device is a mechanism that makes it harder to back out of a decision you've already made. Economists and behavioral researchers have studied these for decades, and the evidence is clear: they work.

Classic examples include automatic 401(k) contributions that require action to stop (rather than action to start), commitment savings accounts with penalties for early withdrawal, and goal-based savings structures where the money can't be touched without a cost.

The core logic is simple. The version of you who decides to save has good intentions. The version of you who is tired and stressed at the end of a hard week might make different decisions. A commitment device protects the first version's choices from the second version's impulses.

This is the design principle behind Bloomin, a locked goal savings app built specifically for people who keep spending their savings before reaching their goal. Users pick a specific goal, like a vacation, emergency fund, or home purchase, contribute money toward it, and the balance gets locked. Completing the goal costs a small 1% fee to unlock. Quitting early costs 25% of the balance.

The penalty is visible before any money is contributed. There's no surprise. The structure is the point.

Bloomin supports up to five active goals at once, which keeps things focused without becoming overwhelming. Each goal has a named type, so the money always has a clear purpose attached to it. The whole design is built around removing easy exits rather than adding more willpower demands.

For people who recognize that their savings problem isn't knowledge but access, that's a meaningful difference.

Putting It Together

Most savings mistakes share a common thread: they assume that good intentions are enough.

They're not, and that's fine. Intentions are a starting point. What turns intention into a finished goal is a system that accounts for human behavior as it actually works, including the parts where motivation dips, impulse hits, and the path of least resistance wins.

The fixes don't require a complete financial overhaul. They're mostly about timing, access, and structure. Save first. Name the goal. Limit the options. Lock the money. Build in a cost for quitting.

Small design changes in how savings work make a much bigger difference than trying harder with the same broken setup.

If any of these mistakes landed close to home, joining the Bloomin waitlist is a useful next step. The app is built specifically for the pattern where the saving part isn't the problem but the not-touching-it part is.