blog

Real Examples of Savings Goals (And How to Actually Reach Them)

A savings goal is a specific target you save toward. Here are real examples, what makes them work, and how to stop spending the money before you get there.

Real Examples of Savings Goals (And How to Actually Reach Them)

A savings goal is a specific financial target you work toward over time. Instead of saving money in a vague, "I should probably be putting something aside" kind of way, a savings goal gives every dollar a job.

A good example: saving $3,000 for a vacation by putting aside $250 a month for 12 months.

That one sentence contains everything a savings goal needs: a clear amount, a clear purpose, and a clear timeline. Most people skip one or more of those things, and that is usually why they never get there.

This post walks through real examples of savings goals, explains what separates the ones that work from the ones that fizzle, and covers what to do when the biggest obstacle is not motivation but the habit of spending the savings before the goal is met.

Table of Contents

- What makes something a savings goal?

- 10 real examples of savings goals

- Short-term vs. long-term savings goals

- What makes a savings goal actually work?

- The biggest reason savings goals fail

- How to save money you cannot easily touch

- How many savings goals should you have at once?

- A simple way to start

What makes something a savings goal?

A savings goal is more than just wanting to have more money. It has three parts:

- A specific purpose. Not "savings" but "emergency fund" or "new laptop" or "down payment."

- A target amount. You need a number to aim at. Without one, you never know when you have arrived.

- A timeframe. Knowing when you want to reach the goal helps you figure out how much to save each week or month.

When all three are in place, a savings goal becomes a plan. When one is missing, it tends to stay a wish.

10 real examples of savings goals

Here are concrete, relatable savings goals with realistic numbers. These are not meant to be exact targets for everyone, because costs vary by location and lifestyle, but they give a useful sense of scale.

1. Emergency fund

Goal: Save $2,000 to $5,000 as a cash cushion for unexpected expenses.

An emergency fund is usually the first savings goal financial advisors recommend, and for good reason. Without one, a single car repair or medical bill can derail everything else. Most people target one to three months of living expenses, though some aim for six months.

This is a goal with no fun payoff, which is why a lot of people deprioritize it. But it is the goal that protects every other goal.

2. Vacation

Goal: Save $2,500 for a week-long trip, including flights, hotel, and spending money.

A vacation goal is one of the most motivating because it has a clear, exciting end result. The typical approach is to decide on the destination, estimate total costs, and divide by the number of months until departure.

For example, a $2,500 trip happening in 10 months means saving $250 a month. Simple math, clear goal.

3. Down payment on a home

Goal: Save $20,000 to $60,000 for a down payment, depending on the home price and loan type.

This is one of the biggest savings goals most people will ever set. It takes years for most people, which means discipline over a long stretch of time. A 20% down payment on a $300,000 home is $60,000. Even a 5% down payment is $15,000. The numbers are large, which makes this goal one of the hardest to protect from lifestyle creep and impulse spending.

4. Car purchase or major repair

Goal: Save $3,000 to $15,000 for a vehicle purchase or a significant repair fund.

Whether saving for a used car outright or building up a repair reserve on top of a car payment, having a vehicle savings goal keeps transportation surprises from wrecking the budget.

5. New baby expenses

Goal: Save $3,000 to $8,000 for the first wave of baby costs including gear, healthcare, and parental leave gaps.

Having a child involves a surge of costs in a short period. Saving ahead means less financial stress when the baby arrives. This is a time-sensitive goal with a built-in deadline, which makes it one of the more urgent ones people set.

6. Education or a professional certification

Goal: Save $1,500 to $10,000 for a course, degree program, or professional certification.

Investing in skills tends to pay off, but it costs money upfront. A savings goal for education avoids the need to put tuition on a credit card, which would turn a smart investment into a costly one.

7. Holiday or celebration spending

Goal: Save $500 to $2,000 for holiday gifts, a wedding, a milestone birthday, or a family celebration.

This is a short-term, very specific goal. The amount is known well in advance. The deadline is fixed. Despite that, most people end up stressed and overspent on holiday gifts every year because they never actually set the goal ahead of time.

8. Tech upgrade or home office setup

Goal: Save $800 to $3,000 for a new laptop, monitor setup, or work-from-home gear.

For freelancers, remote workers, and creators, tools matter. Saving for equipment rather than financing it means no interest and no regret.

9. Moving costs

Goal: Save $1,500 to $5,000 for first and last month's rent, a moving truck, and other relocation expenses.

Moving is expensive in ways people tend to underestimate. Having a savings goal earmarked specifically for a move prevents the financial scramble that comes with a surprise relocation or an opportunity to upgrade living situations.

10. Home repair or renovation

Goal: Save $2,000 to $20,000 for a planned repair or improvement project.

Whether a new roof, a bathroom remodel, or replacing a water heater, home projects cost real money. Homeowners who save ahead avoid the cycle of expensive financing or dipping into emergency funds for predictable expenses.

If you want a clearer map of how goals fit together across time horizons, the post on what are the three types of saving goals breaks that down well.

Short-term vs. long-term savings goals

Not all savings goals work on the same timeline, and understanding the difference matters because it shapes how you save and where you keep the money.

Short-term goals are usually under 12 months. Examples include a vacation, a holiday fund, or a new phone. These tend to live in a regular savings account because you will need the money soon.

Medium-term goals are one to five years out. A car purchase, a home down payment, or funding a certification program usually falls here. These might benefit from slightly higher-yield savings options, though accessibility still matters.

Long-term goals are five or more years away. Retirement savings and a first home down payment in a high-cost city are examples. These are often handled through dedicated investment accounts or retirement plans rather than a standard savings account.

The examples in this post are mostly short to medium-term, because that is where most people get stuck: they set the goal, start saving, and then spend the money before they get there.

What makes a savings goal actually work?

A savings goal that works has a few things going for it beyond just the amount and timeline.

It is specific and named

Vague goals die quickly. "Save more money" is not a goal. "Save $1,200 for a vacation to Mexico in September" is a goal. Naming the goal creates a psychological commitment that a general number does not.

It has a contribution rhythm

Knowing you need to save $300 a month is more useful than knowing you need $3,000 total. Breaking the target into regular contributions makes the goal feel manageable and removes the decision-making overhead from every paycheck.

The money is separated from spending money

This is the part most people skip. Keeping savings in the same account as daily spending makes it too easy to treat the savings balance as a buffer for everyday expenses. Separation creates a small but real barrier.

It has consequences for failing

This sounds harsh, but consequences are what make goals stick. When the only cost of giving up is a vague sense of disappointment, most people give up. When there is a real cost, like a penalty fee or losing a deposit, the behavior changes.

The biggest reason savings goals fail

The most common reason people do not reach their savings goals is not that they do not earn enough or do not care enough. It is that the money stays accessible, and accessible money gets spent.

This is not a willpower problem. It is a design problem.

Research and common experience both point to the same pattern: when money is easy to move, people move it. A good month at work, a slow week of spending, and suddenly the savings account has a decent balance. Then a sale happens, or a dinner out costs more than expected, or the car needs tires, and the savings get tapped. The goal stays in place mentally, but the balance keeps resetting.

The fix is not to try harder. The fix is to make the money harder to reach.

That is the core idea behind a concept called a commitment device, which is a rule or structure that removes easy exits so you do not have to rely entirely on discipline in the moment.

For more on this pattern and practical ways to break it, the post on how to stop touching your savings covers the behavioral side in detail.

How to save money you cannot easily touch

There are a few ways to add friction between yourself and your savings balance. They range from low-effort to high-commitment.

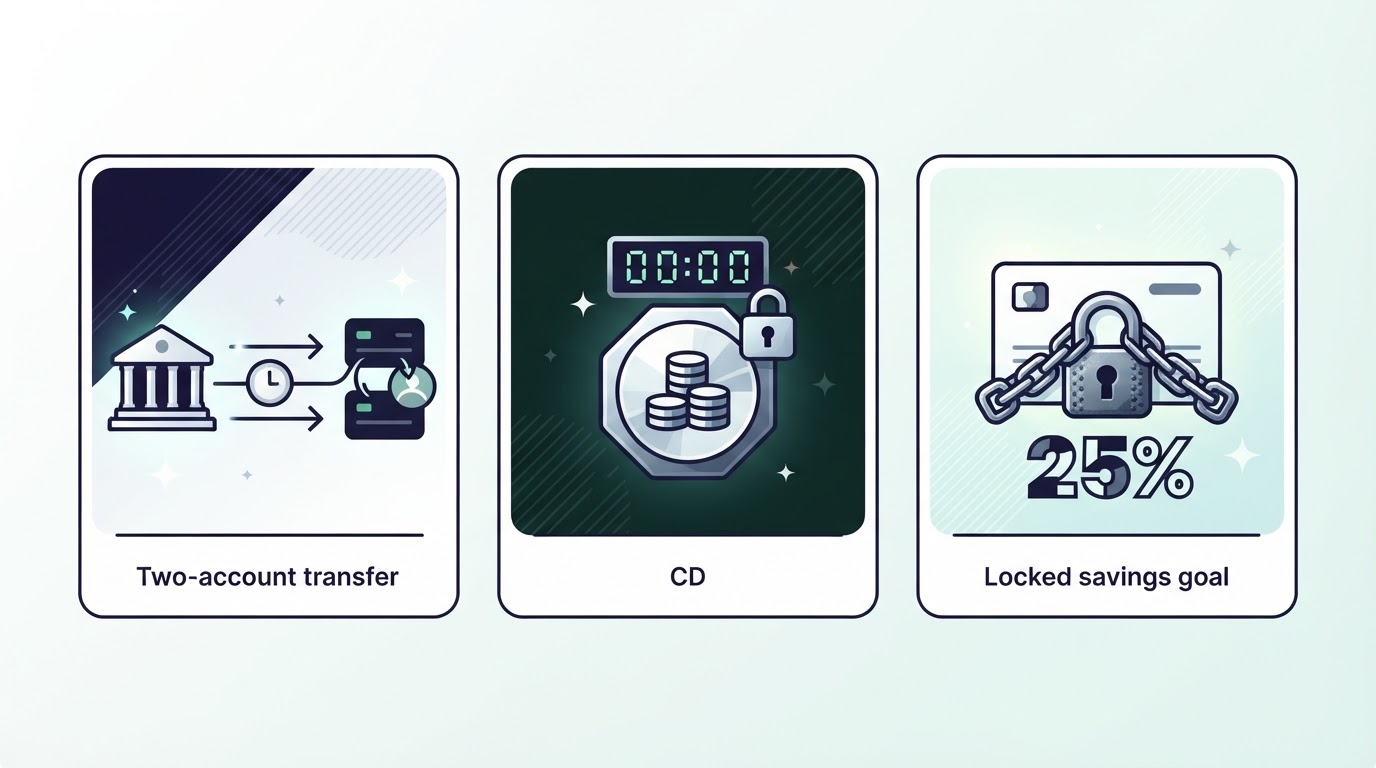

High-yield savings accounts at a separate bank

Opening a savings account at a completely different bank from your checking account adds a small transfer delay, usually one to three business days. That delay is often enough to stop impulse withdrawals. It is a light form of friction, and it costs nothing.

Certificates of deposit (CDs)

A certificate of deposit locks money for a fixed term, usually three months to five years. Withdrawing early means paying a penalty, typically a few months of interest. CDs work well for goals with a fixed end date where you know you will not need the money early.

Employer direct deposit splits

Some employers allow you to split your direct deposit across multiple accounts. Setting up automatic contributions to a separate savings account means the money never hits your checking account in the first place. Out of sight, harder to spend.

Goal-based savings apps with real lock mechanics

Some apps go further than just separating money. They lock the balance and attach a real penalty to early withdrawal, so the decision to quit early has a visible cost.

Bloomin is one example. It is built specifically for people who keep spending their savings before reaching the goal. Users pick a specific goal, like a vacation or an emergency fund, contribute money toward it, and the money gets locked. If you finish the goal, you pay a small 1% unlock fee. If you quit early, you lose 25% of the balance. That consequence stays visible throughout, which is the point. The product is not trying to teach discipline. It is trying to make quitting expensive enough that you think twice.

The goal types in Bloomin map directly to the examples in this post: emergency fund, vacation, new baby, education, vehicle, celebration, home, and tech upgrade. Each goal gets a name before any money moves, so every dollar has a clear purpose from day one.

What is the right savings account for a goal you cannot touch?

A few options come up repeatedly when people search for savings accounts that restrict access.

Certificates of deposit are bank products that lock money for a term. They are FDIC-insured and safe, but the rates can be modest and the terms are fixed. You generally cannot add contributions once the CD is opened, which makes them better for lump sums than ongoing contributions.

Money market accounts offer slightly better rates than standard savings accounts and can include check-writing or debit access. They do not lock money, so discipline still falls on the user.

Dedicated goal savings apps are the most flexible option for people building toward a specific goal over several months. They allow ongoing contributions, show progress toward the target, and in some cases add real friction to withdrawal.

For people who want to understand more about how savings rules and contribution frameworks work, the post on what is the 27 40 rule offers a look at one structured approach to allocating savings by category.

How many savings goals should you have at once?

There is no universal right answer, but most people do better with fewer goals than more.

Having ten active savings goals at once tends to mean that none of them get meaningful contributions. The money gets spread too thin, progress on each goal feels invisible, and motivation fades.

A more effective approach is to pick one to three priority goals and focus contributions there. Once a goal is completed, a new one takes its place.

Bloomin caps users at five active goals simultaneously. That limit is not arbitrary. It is designed to prevent the clutter that happens when saving becomes a list-making exercise rather than actual progress. Keeping the cap visible means users have to decide what matters most before adding a new goal, which is a good habit to develop regardless of what tool you use.

Common mistakes people make when setting savings goals

Even people who understand the basics of savings goals still make a few predictable errors.

Setting a goal with no number. "I want to save for a vacation" is not a goal. "I want to save $2,000 for a vacation" is a goal. The number is what turns an intention into a plan.

Picking a timeline that is too long. Goals that are 24 months away feel abstract. People are better at staying motivated when the goal is close enough to feel real. If you have a long-term goal, break it into milestones.

Mixing savings goals with an emergency fund. The emergency fund is not a savings goal in the traditional sense. It is a foundation. Building toward a vacation with the same money earmarked for emergencies means you will always be raiding one to serve the other. Keep them separate.

Not accounting for irregular expenses. If you know the car registration is due in November or the insurance renews in March, those should be planned contributions, not surprises that derail an existing savings goal.

Treating a savings goal as optional. A goal with a soft commitment gets abandoned at the first sign of inconvenience. If the goal matters, treat contributions as non-negotiable, the same way a rent payment is non-negotiable.

A simple way to start

If the concept of savings goals feels overwhelming, start small and narrow.

Pick one goal. Give it a name and an amount. Pick a regular contribution that fits the current budget, even if it is modest. Open a separate account or use a tool that keeps the money out of reach. And then do not touch it.

The goal does not have to be big. Saving $500 for a small vacation or $300 for a piece of equipment counts as a win if it is the first time you have ever saved all the way to a target without spending it partway through.

What matters is finishing. Finishing one goal builds the habit and the confidence to take on a bigger one next time.

The bottom line

A savings goal is a specific target: a named purpose, a dollar amount, and a timeline. The examples range from a $500 holiday fund to a $60,000 home down payment, and they all follow the same basic structure.

What separates goals that get reached from ones that never do is usually not the goal itself. It is whether the money is protected from easy access long enough to get there.

If the pattern keeps repeating where the savings build up and then disappear before the goal is met, the solution is not more motivation. It is a structure that makes early withdrawal cost something real.

Bloomin is built for exactly that situation. It locks the money, shows the penalty clearly, and removes the easy exit that makes abandoning a goal too tempting. If that sounds like the kind of friction that would actually help, joining the waitlist is the next step.