blog

What Is the 4-3-2-1 Rule for Savings? A Plain-English Guide

The 4-3-2-1 rule splits your income into four buckets. Here's exactly how it works, who it helps, and how to actually stick to it.

What Is the 4-3-2-1 Rule for Savings? A Plain-English Guide

If you've ever searched for a simple framework to stop guessing where your money goes, the 4-3-2-1 rule is one of the cleaner answers out there. It's not a complex spreadsheet method. It's a percentage-based split that tells every dollar what to do before you have a chance to spend it on something you'll regret.

Here's the short answer: the 4-3-2-1 rule says to put 40% of your income toward living expenses, 30% toward wants and lifestyle spending, 20% toward savings, and 10% toward investments or financial goals. Four buckets. Four percentages. Simple math.

But knowing the rule and actually making it work are two different things. This guide covers how it works in practice, how it compares to similar frameworks, where people get stuck, and what to do if you keep raiding your savings bucket before it has a chance to grow.

Table of Contents

- Where the 4-3-2-1 rule comes from

- Breaking down each bucket

- A real-world example

- How it compares to other savings rules

- Who the 4-3-2-1 rule works best for

- The part nobody talks about: actually keeping money in savings

- How to make your savings untouchable

- Common mistakes people make

- Should you follow the 4-3-2-1 rule?

Where the 4-3-2-1 Rule Comes From {#where-it-comes-from}

The 4-3-2-1 rule isn't a government regulation or a certified financial planning standard. It's a budgeting heuristic, meaning it's a practical shortcut that helps most people make better decisions without requiring a finance degree.

Rules like this one have been around for decades in personal finance. The most famous is the 50/30/20 rule, which splits income into needs, wants, and savings. The 4-3-2-1 rule is a variation that breaks things down a little further and pushes the savings and investment slice a bit differently.

The framework gained traction because it's easy to remember and applies to almost any income level. You don't need to track every receipt. You just need to know your take-home pay and do four pieces of basic math.

If you want to see this explained visually with a worked example, this video walks through the rule in a personal budgeting context:

Breaking Down Each Bucket {#breaking-down-each-bucket}

Here's what each number actually means.

40% — Living Expenses (Needs)

This is the biggest bucket and it covers the basics: rent or mortgage, groceries, utilities, transportation, insurance, and minimum debt payments. These are the non-negotiables. The things that happen whether you plan for them or not.

Keeping this at 40% is the discipline point of the whole rule. Most people in high-cost-of-living areas will feel this number is tight. It is. That's intentional. If your housing alone takes 40% of your income, something needs to change, either the housing or the income.

30% — Wants and Lifestyle

Eating out, subscriptions, hobbies, clothes, travel, entertainment. This bucket is for the parts of life that make things enjoyable, not just survivable.

30% feels generous compared to other frameworks, and that's partly why people like the 4-3-2-1 rule. It doesn't expect you to live like a monk. It just puts a limit on the lifestyle spending so the rest of the system holds together.

20% — Savings

This is your emergency fund, short-term goals, and general financial cushion. Vacation funds, a new car, a home down payment, and a three-to-six month emergency buffer all live here.

This is also the bucket most people blow through. The money lands in savings, something comes up (or feels like it did), and then it's gone. The rule puts the number at 20%, but the rule can't stop you from moving money around if the savings account is just a regular account you can dip into whenever.

10% — Investments and Long-Term Goals

The final slice goes toward things with a longer time horizon: retirement accounts, index funds, real estate, or other vehicles that are meant to grow over years, not months.

This number seems small, but compounding over time makes it meaningful. The key is that this money should be the hardest to touch, since it's designed for a future version of you.

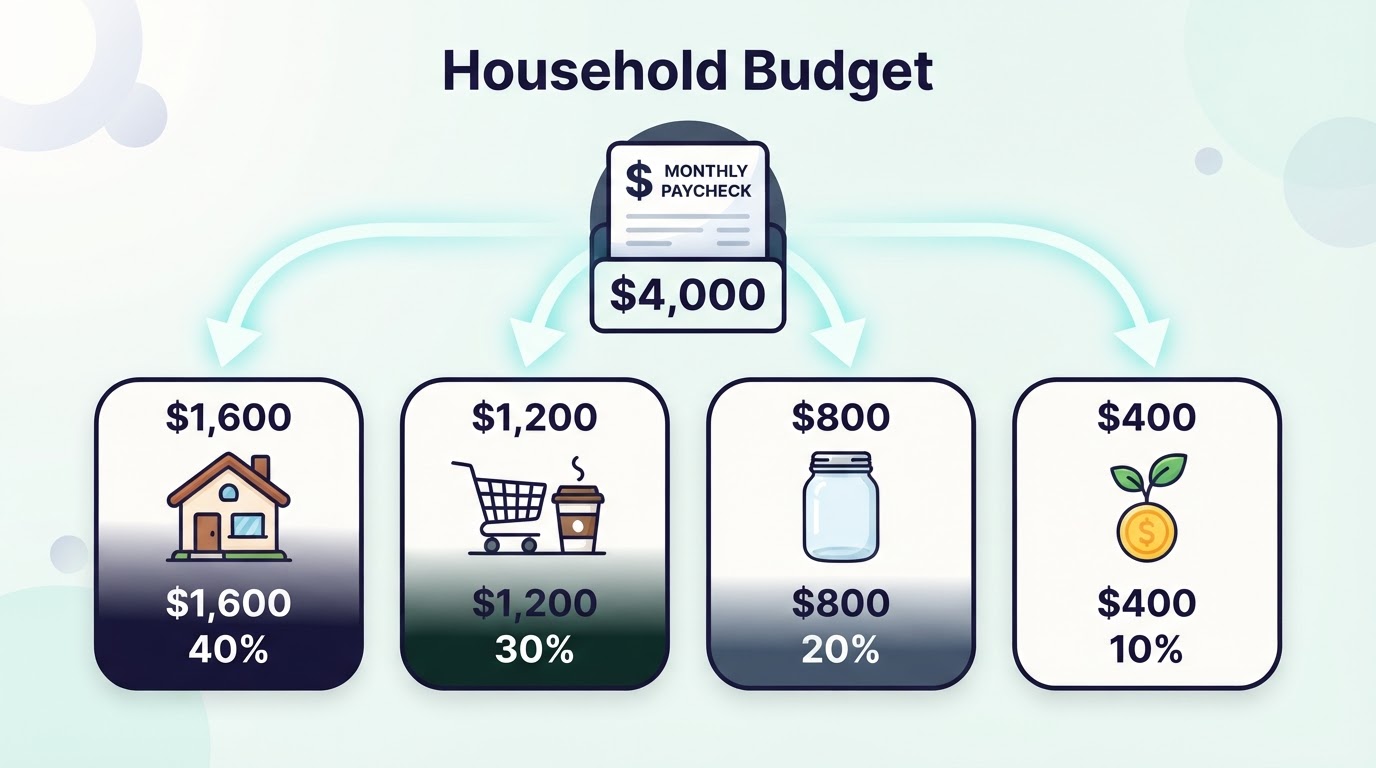

A Real-World Example {#a-real-world-example}

Take someone bringing home $4,000 per month after taxes. Here's how the 4-3-2-1 rule splits that:

| Bucket | Percentage | Monthly Amount |

|---|---|---|

| Living expenses | 40% | $1,600 |

| Wants/lifestyle | 30% | $1,200 |

| Savings | 20% | $800 |

| Investments | 10% | $400 |

So $800 goes into savings each month. In one year, that's $9,600 before any interest. In two years, that's nearly $20,000, which is a serious emergency fund or a meaningful down payment contribution, depending on the goal.

The math isn't complicated. The hard part is the behavior.

If that $800 savings bucket is sitting in an account attached to a debit card, history says it won't last the month. Something comes up: a car repair, a sale that feels too good to skip, a trip someone's going on that sounds fun. Suddenly the savings account is the most convenient ATM in the house.

How It Compares to Other Savings Rules {#how-it-compares}

The 4-3-2-1 rule sits in a family of percentage-based budgeting frameworks. Here's a quick comparison.

50/30/20 Rule

The 50/30/20 rule is probably the most cited framework in personal finance. It puts 50% toward needs, 30% toward wants, and 20% toward savings and investments combined. The 4-3-2-1 rule is similar but separates savings from investments, which helps people with shorter-term goals (like a vacation fund) keep that money distinct from retirement savings.

If you're curious about how other savings frameworks compare, the 27-40 rule is another approach worth understanding before deciding which system fits your life.

70/20/10 Rule

This one puts 70% toward living and lifestyle combined, 20% toward savings, and 10% toward giving or investments. It's a simpler split but doesn't distinguish between needs and wants, which can let lifestyle spending quietly inflate.

80/20 Rule (Pay Yourself First)

This is the most stripped-down version: save 20%, spend 80%. No further breakdown required. It's low friction but also low structure, which works for disciplined people and falls apart quickly for everyone else.

The 4-3-2-1 Rule's Edge

The 4-3-2-1 framework's strength is that it separates four distinct purposes for money. That clarity helps because it forces a decision at the front end. Before anything gets spent, the money already has a label. That's psychologically different from tracking spending after the fact and hoping the numbers work out.

Who the 4-3-2-1 Rule Works Best For {#who-it-works-for}

The rule tends to fit a specific kind of person: someone who wants structure but not a full budget, someone who earns a consistent income and wants a simple system, or someone who's just starting to get serious about saving and needs a framework that doesn't require an app or spreadsheet.

It also works reasonably well for people who are trying to balance saving for multiple goals at once. Because it explicitly carves out both a savings bucket and an investment bucket, you can direct those two slices toward different purposes without blending them.

That said, the rule is not magic. It doesn't account for:

- Very high cost-of-living areas where 40% toward needs is simply not achievable

- Irregular income, where percentages shift month to month

- High debt loads, where debt payments eat into multiple categories

- People who have the rule memorized but still move money between accounts the moment savings accumulates

That last point is where most frameworks quietly fail, and it's worth spending some time on.

The Part Nobody Talks About: Actually Keeping Money in Savings {#the-hard-part}

Knowing a savings rule is easy. Following it for three straight months is where things get messy.

The most common pattern looks like this: someone sets up the 4-3-2-1 split with good intentions, saves $800 in month one, and by week three of month two, that $800 is half gone. Not because of an emergency. Because the money was accessible and the pressure to spend felt urgent enough in the moment.

This isn't a discipline failure, at least not in the way most budgeting content frames it. It's a structural problem. If savings sits in an easy-access account, the cost of spending it feels low. There's no friction. There's no consequence visible enough to slow the decision down.

Research in behavioral economics has a name for this: present bias. People consistently overvalue what they can have right now compared to what they'll benefit from later. The 4-3-2-1 rule tells you the right percentages, but it doesn't solve present bias. That requires a different kind of tool.

You can read more about the specific mechanics of how to stop touching your savings if this pattern sounds familiar.

How to Make Your Savings Untouchable {#make-savings-untouchable}

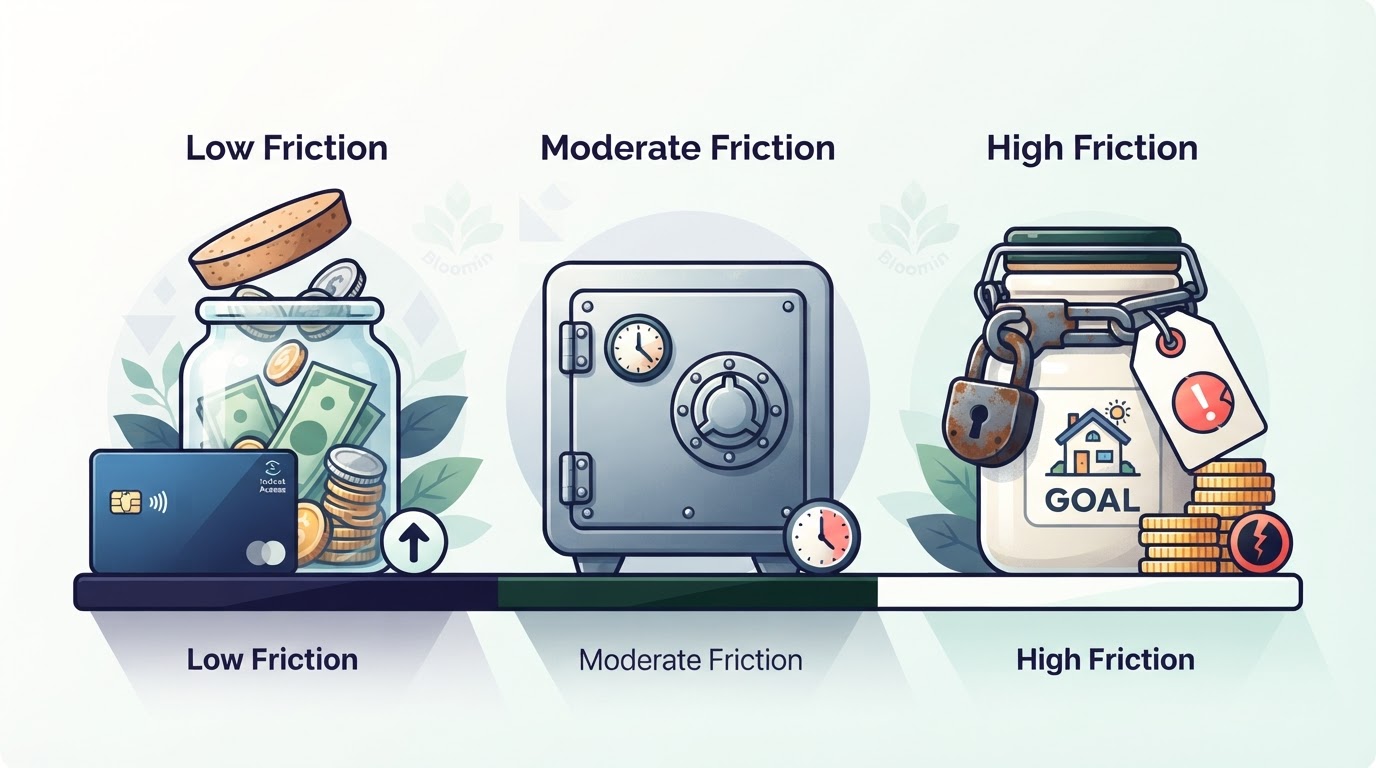

The solution to present bias is friction. The harder it is to access savings, the less often people do it. This is why certain savings structures tend to work better than others for people who struggle with this.

High-Yield Savings Accounts at a Separate Bank

Opening a savings account at a completely different institution than your checking account adds a small amount of friction. Transfers take one to three business days. That delay is often enough to let the impulse cool down before the money moves.

Certificates of Deposit (CDs)

A CD locks money for a fixed term, typically three months to five years. Early withdrawal comes with a penalty, usually a few months of interest. The consequence is real but relatively small. For people with moderate discipline, a CD is often enough of a speed bump. For people who've already raided CDs mid-term, it clearly isn't.

Goal-Based Locked Savings Apps

A newer category of tools takes the locked-savings concept further by attaching real consequences to early withdrawal. These aren't just CDs with a mild penalty. The apps are specifically designed for people who identify as someone who can't stop touching their savings.

Bloomin is one such app. It works by letting users pick a specific savings goal, contribute money toward it, and then lock that money so it's genuinely hard to access. The consequences are clear before any money moves: complete the goal and pay a 1% unlock fee, or quit early and lose 25% of the balance.

That 25% early-exit penalty is meaningful. It's not a gentle nudge. It's a consequence that makes the cost of impulsive spending visible in a way that a normal savings account simply doesn't.

For someone who's tried the 4-3-2-1 rule and found that the savings bucket always gets raided, a structure like this directly addresses the root problem. The rule tells you what percentage to save. The locked account makes sure it actually stays there.

Bloomin also supports up to five active goals at once, which maps nicely onto the 4-3-2-1 framework. The 20% savings slice could fund multiple named goals simultaneously: an emergency fund, a vacation, and a home down payment, each in its own locked bucket.

Common Mistakes People Make with the 4-3-2-1 Rule {#common-mistakes}

Even people who understand the rule well tend to run into the same problems. Here are the most common ones.

Treating Percentages as Suggestions

The 4-3-2-1 rule only works if the percentages are treated as a system, not an aspiration. People who round up the wants category "just this month" and plan to make up for it later almost never do. The month passes, and the next month starts from a similar place.

Leaving Savings in an Accessible Account

Already covered above, but worth repeating: the savings bucket and the investment bucket should both be structurally separated from everyday spending money. Keeping everything in one bank account is like putting a candy bowl on your desk and hoping you don't eat from it.

Not Naming the Savings Goal

Generic savings is easier to spend than specific savings. "My emergency fund" or "Barcelona in October" is harder to raid than a line item called "savings." This is why naming goals matters, not just setting a number. For more on this, the article on the three types of saving goals breaks down how different goal structures affect savings behavior.

Applying the Rule to Gross Income Instead of Net

This is a math error more than a behavior problem. If someone earns $5,000 gross but takes home $3,800 after taxes and deductions, applying the rule to $5,000 will result in categories that don't add up in real life. Always use take-home pay.

Expecting the Rule to Work Without Structure

A rule is just a rule. It doesn't move money, lock accounts, or stop transfers. People who get the most out of percentage-based frameworks are those who automate or structurally separate each bucket the moment income arrives. The more manual the process, the more likely it falls apart.

Should You Follow the 4-3-2-1 Rule? {#should-you-follow-it}

For most people with a stable income who want a simple, memorable framework, the 4-3-2-1 rule is a solid starting point. It's more nuanced than the 50/30/20 rule because it separates savings from investments, which helps when you're juggling short-term and long-term goals at the same time. It's simpler than zero-based budgeting, which requires accounting for every dollar every month.

The rule fits well if:

- Income is fairly predictable month to month

- The goal is to start saving consistently without building a complex system

- There's a mix of short-term goals (vacation, emergency fund) and long-term goals (retirement, investments)

- A framework is needed more than a detailed tracker

It fits less well if:

- Housing costs alone already exceed 40% of take-home pay

- Income varies significantly month to month

- Debt payments are significant enough to complicate the math

- The savings bucket keeps disappearing before goals get funded

That last scenario is the most common reason people switch from a budgeting rule to a structural savings tool. The rule is fine. The behavior is the problem. And behavior problems generally need structural solutions, not more information about the right percentages.

Putting It All Together

The 4-3-2-1 rule is a practical, easy-to-remember framework that gives every dollar a home. Forty percent toward needs, 30% toward lifestyle, 20% toward savings, and 10% toward investments. It's not perfect for every situation, but it's a genuinely useful starting point for anyone who wants to get more intentional about where their income goes.

The bigger challenge, for most people, is the savings and investment buckets. Knowing the rule doesn't stop the impulse to dip into those slices when money feels available. That's where structural tools matter more than knowledge.

If the 20% savings slice keeps disappearing before it becomes something meaningful, the issue isn't that you don't know the rule well enough. It's that the money is too easy to reach. Putting it somewhere it actually stays, with a real cost for pulling it out early, is often the only thing that changes the outcome.

If that pattern sounds familiar, Bloomin is worth a look. It's built specifically for people who've tried saving with good intentions and found that easy access is the enemy. The app locks contributions toward named goals, keeps the finish fee and the early-exit penalty visible at all times, and removes the easy exit that tends to undo everything else.

You can join the waitlist to get early access when the first product wave opens.

The 4-3-2-1 rule tells you how to think about your money. A locked savings structure helps make sure you actually follow through.